April 2024

Spring activity boost pushes asking prices close to new record

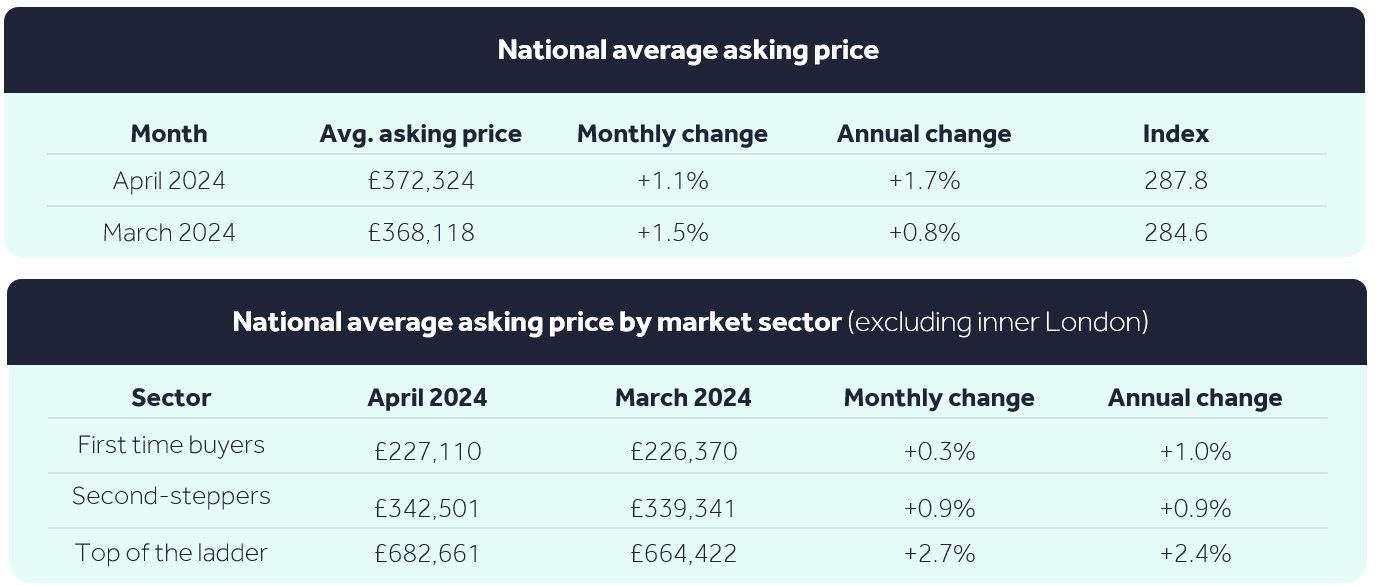

- The average asking price of property coming to the market rises by 1.1% (+£4,207) this month to £372,324, just £570 short of the record in May 2023, while the annual rate of price growth is now +1.7%, the highest level for 12 months:

- A key factor behind this growth towards a near-record average price is the largest homes, top-of-the-ladder sector, which is seeing its strongest start to the year for price growth since 2014

- However, the market remains price-sensitive, and operating at different speeds, with prices and activity rising more slowly in the more mortgage dependent first-time buyer and second-stepper sectors

- The number of new sellers coming to the market is up by 12% compared to this time a year ago, and the number of sales being agreed is up by 13% as both seller and buyer activity rebound from last year’s much more subdued Spring:

- The biggest growth in activity is taking place in the largest homes, top-of-the-ladder sector, with the number of new sellers up by 18% compared with last year, and the number of sales being agreed up by 20%

- Home-owners are springing into action, with Thursday 28th March seeing the highest number of new sellers coming to the market in one day so far in 2024, and the third largest since August 2020

- There appears to be a window of opportunity for those considering a move to act, with a busy summer of sporting events, followed by a likely General Election, creating more home-mover distractions than usual

Average new seller asking prices rise by 1.1% this month (+£4,207) to £372,324, a substantial monthly price increase, but in line with the ten-year average for this time of year. The average price of property coming to the market for sale is now just £570 short of May 2023’s record of £372,894, while the annual rate of price growth increases to 1.7%, the highest level for 12 months. A key driving factor behind this growth towards a near-record average asking price is the largest homes, top-of-the-ladder sector, which is seeing its strongest start to a year for price growth since 2014. Overall, it continues to be a much-improved first four months of the year compared to 2023, with the market seeing boosts in both buyer and seller activity this Spring. However, agents report that despite the rise in prices and general sense of greater optimism, high mortgage rates are continuing to stretch affordability for the typical buyer. The market remains very price-sensitive and operates at different speeds across its many segments and areas, with prices and sales activity rising more slowly in the more mortgage-dependent, mass-market first-time buyer and second-stepper sectors.

“The top-of-the-ladder sector continues to drive pricing activity at the start of the year, with movers in this sector typically less sensitive to higher mortgage rates, and more equity rich, contributing to their ability to move. While some buyers, across all sectors, will feel that their affordability has improved compared to last year due to wage growth and stable house prices, others will be more impacted by cost-of-living challenges and stickier than expected high mortgage rates. Despite these factors, it has been a positive start to the year in comparison to the more muted start to 2023. However, agents report that the market remains very price-sensitive, and despite the current optimism, these are not the conditions to support substantial price growth. Sellers who are keen to secure their sale will still need to price realistically for their local market and avoid being overambitious at the start of marketing to give themselves the best chance of finding a buyer.”

Tim Bannister Rightmove’s Director of Property Science

The number of new sellers coming to the market is up by 12% compared to this time a year ago, while the number of sales being agreed is up by 13%, as the market rebounds from a much more subdued Spring last year. Much of this activity is occurring in the top-of-the-ladder sector, which covers four bed detached houses and all five-bed properties and higher, with the number of new sellers in this sector up by 18% compared to this time last year, and the number of sales agreed up by 20%. Agents report that the increased choice in this sector after many months of very limited supply, is encouraging previously reticent home-owners to come to market, creating a cycle of more new listings leading to more sales activity.

By contrast, activity is rising more slowly in the mass-market, more mortgage-dependent first-time buyer and second-stepper sectors, which makes up the majority of the market. The number of new sellers in both sectors is up by 10%, while the number of sales agreed is up by a more modest 9% and 13% respectively compared with last year. Mortgage rates are remaining high for longer than some expected at the start of this year, which is likely having a greater impact on movers in these sectors.

Overall, the number of sales being agreed is now level with 2019 despite buyer conditions being much more challenging, with the average five-year mortgage rate now at 4.84%, compared with 2.45% in April 2019, while average property prices are 22% higher. However, affordability has been assisted by average wage growth of 27% over this time-period, slightly ahead of house price growth.

Emphasising this year’s boost in Spring buyer and seller activity, Thursday 28th March saw the highest number of new sellers coming to the market in one day so far in 2024, and the third largest since August 2020 – only pipped by Boxing Day 2022 and 2023 – with many sellers keen to capture buyer attention over the Easter weekend.

“The summer holidays are typically a time of distraction for some home-hunters, as they temporarily pause their search and head abroad or to the British seaside. In addition, the Euro 2024 football tournament and the Olympics this summer, likely followed by a General Election during the second half of the year, will add more buyer distractions than usual. There appears to be a tempting window of opportunity for those who are considering a move to act now before these distractions arrive. While affordability is still very tight, property and mortgage market conditions remain stable, buyer choice is good, and many sellers will recognise that it is the right time to negotiate on price to agree a deal. The boost in activity suggests that many home movers are already springing into action to make their move.”

Tim Bannister Rightmove’s Director of Property Science

Agents’ Views

“We’re seeing an increase in ‘for sale’ and ‘sold’ signs in most areas and our own figures point to a successful first quarter. Applicant registrations are up 20% compared to Q4 2023. New instructions have increased too, but by a lower percentage, showing that the supply and demand gap is beginning to narrow. For those looking to buy or sell, now is the ideal time to put plans into action.

“Inflation falling to 3.2% in March suggests a Bank of England interest rate cut would be welcome sooner rather than later.

“Those wishing to achieve a quick sale should continue to be realistic about prices. The months leading up to the general election, likely to be in the Autumn, may see a short-term pause in activity in the market. And the outcome of that election – and its impact on house prices and activity – is far from certain.”

Kevin Shaw, National Sales Managing Director at Leaders Romans Group

“2024 is off to a good start with more properties coming on and more sales happening. Going into the end of Spring, this will hopefully continue as inflation drops and the possibility of a Base Rate reduction is on the horizon. Price sensitivity is still an issue, and sellers need to be realistic in their pricing strategy and manage their expectations. The health of the property market is primarily gauged on the number of properties listed and sold, and it’s good to see these metrics improving compared with last year.”

Jim Parker, Managing Director at Fife Properties

Regional Trends

Price & Activity Trends

London Trends

Affordability Trends

The first-time buyer monthly mortgage payment is based on Bank of England data of the averages for 90% LTV two-year fixed mortgages from lenders, and the average asking price of a typical first-time buyer home (two bedrooms or fewer) using the Rightmove House Price Index. The equivalent monthly rent is calculated using the same property types (two bedrooms or fewer).

The affordability to buy a first home is based on the Average Weekly Earnings (AWE) dataset from ONS multiplied by 4.5 to get the typical maximum that a person can borrow from a lender. The average asking price of a typical first-time buyer home is taken from the Rightmove House Price Index.

Full Report

Upcoming Dates

20th May

17th June

15th July

19th August

16th September

21st October

18th November

16th December